For 42% of Canadians, financial stress tops the worry list.

Money doesn’t just make the world go ‘round, it makes the world go wild with worry

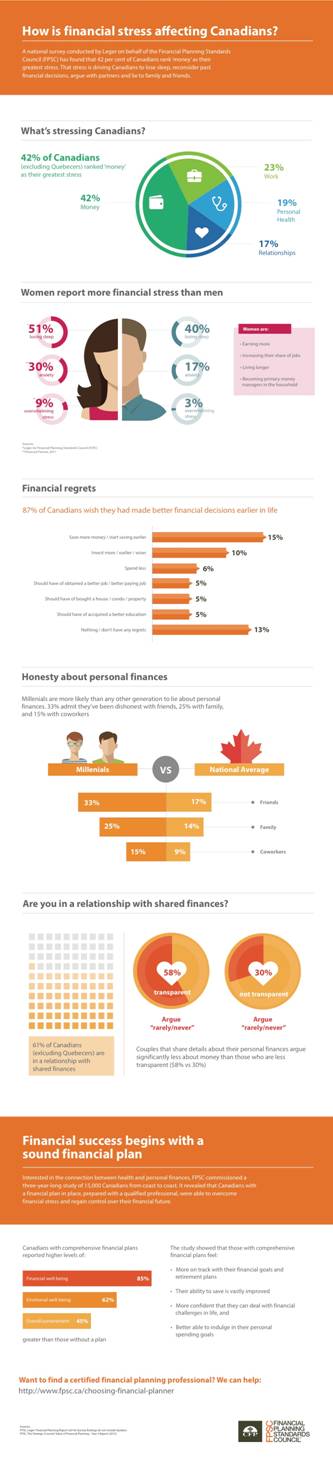

Consider the stats that came with a recent Financial Planning Standards Council (FPSC) study. They show that financial stress tops the worry list of 42 per cent of Canadians (excluding Quebecers). Relationships, regrets, and dishonesty bearing on personal finance figure into the statistical picture as well.

The study shows that 51 per cent of females are losing sleep over finances compared to 40 per cent of males.

Thinking about the 42 per cent figure, I realize it translates to many millions of flesh-and-blood adults in our country.

Women fare worst among the distressed. The FPSC study shows that 51 per cent of females are losing sleep over finances compared to 40 per cent of males. Meanwhile, 30 per cent of women are anxious about money compared to 17 per cent of men. Nine per cent of women and three per cent of men report feeling overwhelmed by financial stress.

Couples who share details about their personal finances argue significantly less about money …

Relatedly concerning couples, 61 per cent of all people sampled (excluding Quebecers) report being in a relationship with shared finances. Interestingly, especially from our point of view at Credit Canada Debt Solutions, “couples who share details about their personal finances argue significantly less about money than those who are less transparent (58% vs 30%).”

Across the board for women and men, financial stress outranks other life concerns by big margins. Stress rankings relating to work, personal health, and relationships came in at 23 per cent, 19 per cent, and 17 per cent respectively.

“Millennials are more likely than any other generation to lie about personal finances …”

Then there are the figures concerning regrets and dishonesty relating to money.

As the FPSC reports: 87 per cent of Canadians wish they had made better financial decisions earlier in life (most had misgivings about failing to save and invest properly). Meanwhile, the findings show that, “Millennials are more likely than any other generation to lie about personal finances: 33% admit they've been dishonest with friends; 25% with family; and 15% with coworkers.”

“Canadians with a financial plan in place were able to overcome financial stress and regain control …”

What is one to make of all this? Well, first of all the FPSC offers fact-based words of wisdom. After commissioning a national, three-year study into health and personal finance, the council found that, “Canadians with a financial plan in place – prepared with a qualified professional – were able to overcome financial stress and regain control over their financial future.”

Solutions to ending money-related worries are readily at hand for Canadians from all walks of life.

The study showed that those with comprehensive financial plans feel:

• More on track with their financial goals and retirement plans;

• Their ability to save is vastly improved;

• More confident that they can deal with financial challenges in life; and

• Better able to indulge in their personal spending goals.”

Be aware that solutions to ending money-related worries are readily at hand for Canadians from all walks of life, at all income levels. I speak from experience as head of a credit counselling agency that for 50 years has helped financially stressed families and individuals take control of their money, their debt, and their lives.

I urge Canadians to reach out to non-judgmental professionals in times of trouble.

In most cases at Credit Canada, we find money problems usually involve one or more factors: people deny the reality of their financial circumstances; they are uncommunicative about their difficulties (often feeling shame); they fail to set and evaluate financial goals; they lack the personal money management skills to act decisively.

I urge Canadians to reach out to non-judgmental professionals in times of trouble. Understand that whether you’re facing crippling debt problems or even moderate ones, qualified credit counsellors can help you dash money worries for long-term peace of mind. At Credit Canada, we do it through not-for-profit debt consolidation and financial literacy programs, and through programs currently in development.

New digital programs that broaden E-learning courses based on our extensive “Financial Coaching Series.”

Right now Credit Canada is preparing to implement affordable new interactive programs that broaden E-learning courses based on our extensive “ Financial Coaching Series,” which is designed to turn financial worriers into financial wizards. The first of these learning modules are being rolled out this spring in league with one of Canada’s leading financial institutions.

Looking ahead, we hope to roll out E-learning courses extensively within a national framework of financial industry stakeholders, community partners, and ordinary households, making a good night’s sleep a ready possibility for all Canadians.

Here I ought to make it clear that while Credit Canada works with levels of government to forward the cause of financial education, we do not supply government debt relief or government debt programs. We are an independent, not-for-profit agency in good standing as an accredited charter member of the Ontario Association of Credit Counselling Services (OACCS), and the Canadian Association of Credit Counselling Services (CACCS).

Frequently Asked Questions

Have questions? We are here to help.

What is a Debt Consolidation Program?

A Debt Consolidation Program (DCP) is an arrangement made between your creditors and a non-profit credit counselling agency. Working with a reputable, non-profit credit counselling agency means a certified Credit Counsellor will negotiate with your creditors on your behalf to drop the interest on your unsecured debts, while also rounding up all your unsecured debts into a single, lower monthly payment. In Canada’s provinces, such as Ontario, these debt payment programs lead to faster debt relief!

Can I enter a Debt Consolidation Program with bad credit?

Yes, you can sign up for a DCP even if you have bad credit. Your credit score will not impact your ability to get debt help through a DCP. Bad credit can, however, impact your ability to get a debt consolidation loan.

Do I have to give up my credit cards in a Debt Consolidation Program?

If you enter a DCP in Canada, you will have to refrain from using credit, which includes unsecured credit cards; however, you can still use a secured credit card. Once you've successfully completed the program, you may be eligible for an unsecured credit card.

Will Debt Consolidation hurt my credit score?

Most people entering a DCP already have a low credit score. While a DCP could lower your credit score at first, in the long run, if you keep up with the program and make your monthly payments on time as agreed, your credit score will eventually improve.

Can you get out of a Debt Consolidation Program?

Anyone who signs up for a DCP must sign an agreement; however, it's completely voluntary and any time a client wants to leave the Program they can. Once a client has left the Program, they will have to deal with their creditors and collectors directly, and if their Counsellor negotiated interest relief and lower monthly payments, in most cases, these would no longer be an option for the client.

Editorial Staff • Author

X

Related Articles

Practical Tips on How to Deal With Financial Stress in Canada

Money stress has a way of following you everywhere: it can affect your sleep, your relationships, and your ability to concentrate at work. You're not imagining it, and many ...

I Made a Bad Financial Decision: What Now?

Have you ever kicked yourself after a bad financial move? We’ve all been there. Whether it’s an extravagant purchase on your credit card that you regretted later or a poor stock ...

The Surprising Link Between Finances and Mental Health

You’ve heard the phrase “money can’t buy happiness.” The phrase is nuanced by related results of money, like better access to personal care, shelter, entertainment, food, and ...