Frequently Asked Questions

Have questions? We are here to help.

As Credit Counsellors, we’re often asked, can you consolidate debt into a mortgage? The thought is that in doing so, you will reduce the overall interest you have to pay on your individual debts (because the mortgage rate should be lower) and free up potentially hundreds of dollars every month.

It’s a win-win, right? Not so fast.

Sometimes, consolidating debt into a mortgage can cost you. But first, let’s take a look at just how it works.

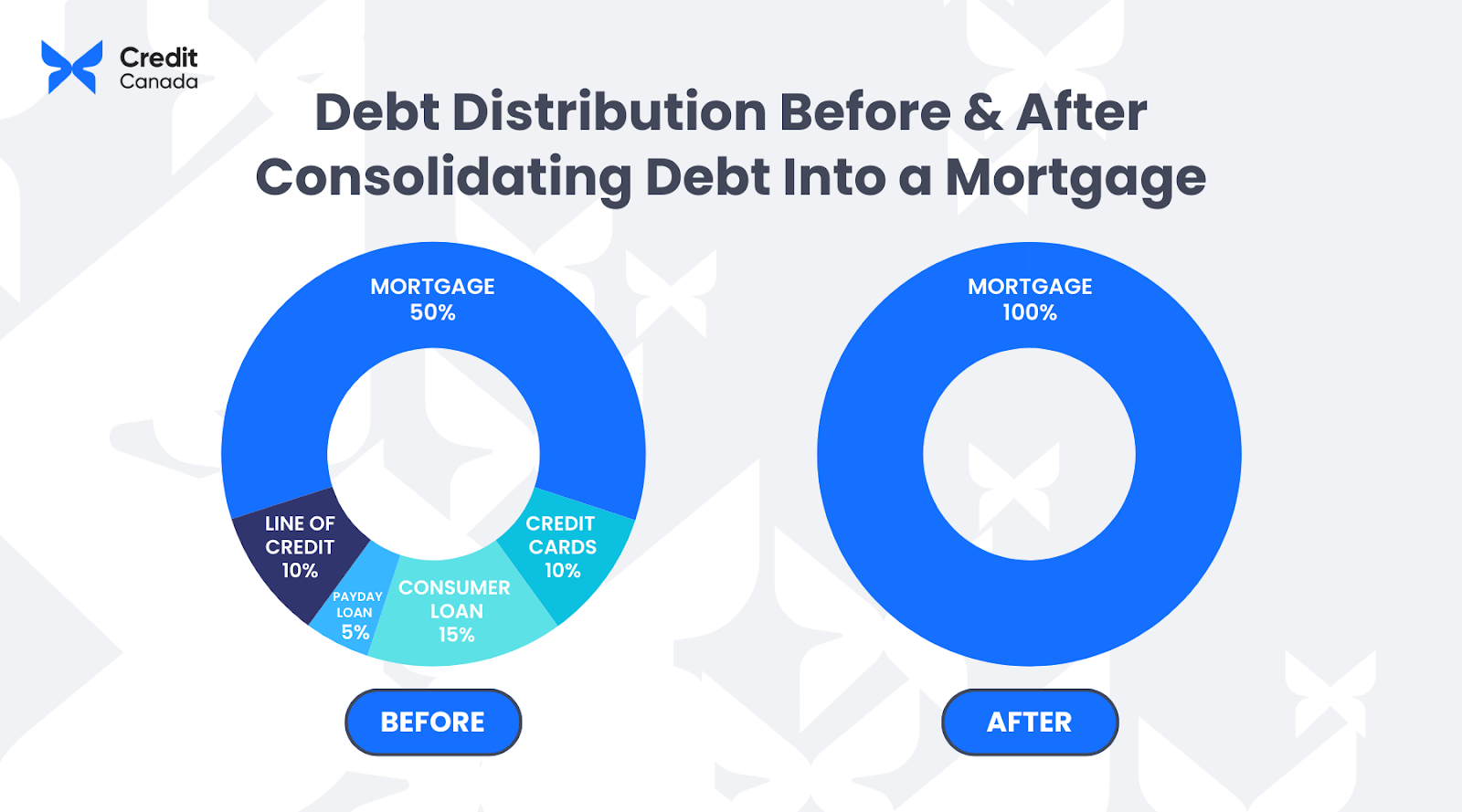

Debt consolidation is the practice of taking multiple sources of debt and combining them into a single account. When it comes to consolidating debt into a mortgage, this often means rolling your current mortgage agreement and your high-interest debts (such as credit card debt, payday loans, and other non-mortgage balances) into a new mortgage set at a new (hopefully lower) interest rate. This is possible because most homes have equity in them. Equity is the difference between the value of the home and what is owed on the mortgage.

For example, say your home is worth $700K and you only owe $500K on the mortgage. That means you have $200K worth of equity. Even better, as you continue to pay down your mortgage, equity continues to go up (a spike in property value also increases it, while a drop in property value, of course, decreases it). That $200K is a nice chunk of change, right? So in this case, you might consider using it to pay down some of your high-interest balances by choosing to consolidate your debt into a mortgage that you refinanced.

Once you’ve done this, your mortgage debt will increase by the amount of non-mortgage debt you rolled into it, plus the cost of breaking the old mortgage (if applicable). The upside is that, in theory, the interest you pay on your non-mortgage debt will decrease.

Want to know your debt options? Take our quick and easy debt assessment quiz to find out how you can manage and reduce your debt.

Figuring out whether a debt consolidation mortgage will benefit you in the long run depends on many factors. Every mortgage is unique, and there are just too many variables to provide a black-and-white answer—it's all grey!

For example, some people will have to consider whether they can even qualify for a new mortgage for consolidating debt depending on the latest rules around mortgages today. You also have to consider the new mortgage rate you can get on the renewal. Will it be more or less than your current rate? If it's more, does the decrease in interest that you'll pay on your non-mortgage debts outweigh the increase in the mortgage interest you'll end up paying? Before you consolidate your debt into a mortgage, these are all questions you really need to consider!

There's also the cost of the penalty for breaking your current mortgage, as well as any legal fees involved. In some cases, your property might need to be assessed, and that will cost you some money too.

These are all things you'll need to think about to really know if consolidating debt into your mortgage is the best choice for you. If you want to know what the impact of choosing to consolidate debt into mortgage payments will look like for you specifically, you might want to consider speaking with your bank or credit union, as well as a mortgage broker who will provide an overall picture of available options based on your financial situation.

What if you’re not a current homeowner, but are thinking about buying a home? You may be able to consolidate your debt into a mortgage when purchasing a new home. To be eligible, lenders will look at your loan-to-value (LTV) ratio to determine the risk you pose as a borrower. LTV is the size of your loan compared to the value of the home you intend to buy.

So, if your LTV is under a certain amount (typically 80% or less) your lender may allow you to roll high-interest balances into your lower-interest home loan. This can be a great way to get out from under high-interest-rate loans or credit cards.

There can be many benefits to using mortgage consolidation and refinancing to move your unsecured, high-interest debts into your mortgage — in some cases, you could save a couple of hundred dollars a month over the life of your mortgage! But it also has its downsides.

Consolidating debt into your mortgage can be a smart move because it often means lower interest rates. This can save you money in the long run by reducing the amount you pay in interest each month.

Another benefit of rolling your debt into your mortgage is simplified payments. Instead of juggling multiple bills with different due dates and interest rates, you'll have just one easy-to-manage payment each month.

Consolidating your debt into your mortgage can boost your cash flow by reducing your monthly payments. With lower interest rates and potentially longer repayment terms, you'll have more income each month to cover essential expenses or save for the future.

By rolling other debts into your mortgage, you’ll be paying them off over a longer period of time, so you won't be debt-free any sooner.

Some people begin seeing their home as a resource they can tap into whenever they need it. In some cases, they’ll even start treating their home like it's an ATM. But equity is not an unlimited resource. If you use up your home equity, you may not have any left when you really need it, such as during a job loss or medical emergency.

According to Equifax Canada’s consumer credit trends and insights report, Canadian consumer debt rose to $2.4 trillion in 2023. With an average debt load of approximately $21,131 (excluding mortgages), the data revealed Canadians are using credit cards more–and consolidating debt with a mortgage doesn't always help curb spending.

Many people continue to use their credit cards after consolidating their balances into their mortgage. So now, not only are they paying more on their mortgage, but they’ll also be back in the hole with credit card companies.

Of course, there’s also no guarantee you'll qualify to consolidate non-mortgage debt into your mortgage. If you’re wondering, “How much can I borrow against my home,” every lender is different and every borrower is different. Deciding when it makes sense to consolidate debt into your mortgage typically depends on the value of the home, how much debt you're looking to consolidate into your mortgage, and how much equity you have in the home. Even if your credit score is not the best, don't let this hold you back from exploring this option.

So, before you follow any ads that pop up after typing in something like “mortgage consolidation” or “consolidating debt into a mortgage in Canada,” it’s important to do some research or even speak with a financial advisor or debt management counsellor. Mortgage brokers can help in many situations where you think there is no hope.

Ready to take charge of your debt? Our Debt Management services provide the support and guidance you need. Get Started.

If you're considering rolling your debt into your mortgage but aren't sure where to start, here's how to navigate the process:

First, it’s important to take a hard look in the mirror and assess your current financial situation. Take stock of your debts (including their amounts and interest rates), check your credit score, and evaluate your home equity. This will give you a better understanding of whether consolidation is an option.

Next, be sure to research what mortgage options are available to you so you can find the best fit. Consider factors such as interest rates, repayment terms, and any associated fees. It’s important to take time to compare products from different lenders to ensure you make an informed decision that aligns with your financial goals.

Before signing a new consolidation mortgage or refinancing an existing mortgage, consult with a financial professional. At Credit Canada, our Credit Counsellors can provide personalized, expert advice tailored to your situation and can help you navigate the complexities of debt consolidation. A mortgage advisor can also assist in selecting the most suitable mortgage product and guide you through the application process.

Once you've chosen the right mortgage product for you, carefully follow the lender's instructions for the application process and provide all necessary documentation. Be prepared for a thorough review of your financial history and assets by the lender.

Finally, upon consolidating your debts, use the newly available funds wisely to maximize their impact. Consider focusing on building an emergency fund, investing in retirement savings, or tackling any remaining debts not included in the consolidation.

If you’re hesitant to use up some of your home equity to pay off your debts, that’s understandable. Fortunately, there are a number of alternatives to getting a debt consolidation mortgage you may want to consider. Our debt consolidation calculator can give you a rough idea of how long it will take you to pay off your unsecured debts at their current interest rates using different repayment strategies. The calculator also provides different debt relief options that may be available to you rather than consolidating your debt into your mortgage.

Not sure how much you owe or how long it’ll take to pay off? Try our free debt repayment calculator to get a clearer sense of your situation and repayment options.

Similar to a home equity loan, but instead of getting a lump sum a HELOC is a revolving line of credit (similar to a credit card). That means you have access to a certain amount of money that you can use as needed, only paying interest on what you borrow.

The downside is that HELOC interest rates are variable, meaning they could go up and, as with a home equity loan, undisciplined spenders may tap out their home equity.

If you’re not keen on borrowing against your home, you may be able to get a debt consolidation loan through a bank, credit union, or finance company. A debt consolidation loan can be used to pay off unsecured debts, leaving you with only one monthly payment to a single lender, hopefully at a lower interest rate.

However, to obtain a debt consolidation loan you must have good credit, collateral, or a co-signer with good credit. In some cases, a stable source of income is also needed.

As with home equity loans and HELOCs, some people can run into trouble if they continue to use their credit cards, while also owing to the debt consolidation loan lender. However, this may be preferable to signing a new consolidation mortgage or refinancing an existing mortgage to cover high-interest balances for some.

Struggling to manage multiple debts? Our Debt Consolidation Program can help you combine them into one easy monthly payment. Learn More.

Okay, this isn’t a debt consolidation option, but we’d be remiss not to include it! Often, rather than continuing to borrow, people can get a handle on their debt by practicing better money management skills. This includes budgeting and watching how you spend your money. You can do this online with our free, downloadable Budget Planner – it’s easy to use and the instructions are included in the spreadsheet.

If a debt consolidation mortgage and the other options mentioned above don’t interest you, or you think poor credit will hold you back, a Debt Consolidation Program is another great debt relief option.

A Debt Consolidation Program involves rolling all of your unsecured debt into one monthly payment through a non-profit credit counselling agency like Credit Canada. A certified Credit Counsellor will then contact your creditors, on your behalf, to lower your monthly payment and reduce or stop the interest on your debt.

The best part is that you don't need good credit to qualify for a Debt Consolidation Program. All you need to focus on is making your new, lower monthly payment every month on time and in full. Our team can also provide you with guidance on how to rebuild your credit and manage your money. It's a win-win across the board and a great alternative to consolidating debt into your mortgage. You can hear from some of our clients here!

If you're looking for some free expert advice on what might be the best debt relief option for you given your financial situation, give us a call at 1.800.267.2272 and have a free counselling session with one of our certified Credit Counsellors. You'll get all the information you need to make the best decision for you!