Practical Tips on How to Deal With Financial Stress in Canada

Financial stress is a normal reaction to real economic pressure, not a personal failing, and it's affecting more than half of Canadians right now.

Financial stress and financial anxiety are different: stress is triggered by a specific situation, while anxiety is a persistent worry that lingers even when things are stable.

Practical steps like building a budget, growing an emergency fund, and paying down high-interest debt can meaningfully reduce financial stress over time.

If stress is costing you sleep, straining your relationships, or leaving you with no clear path out of debt, free and confidential support from a certified Credit Counsellor is available to all Canadians.

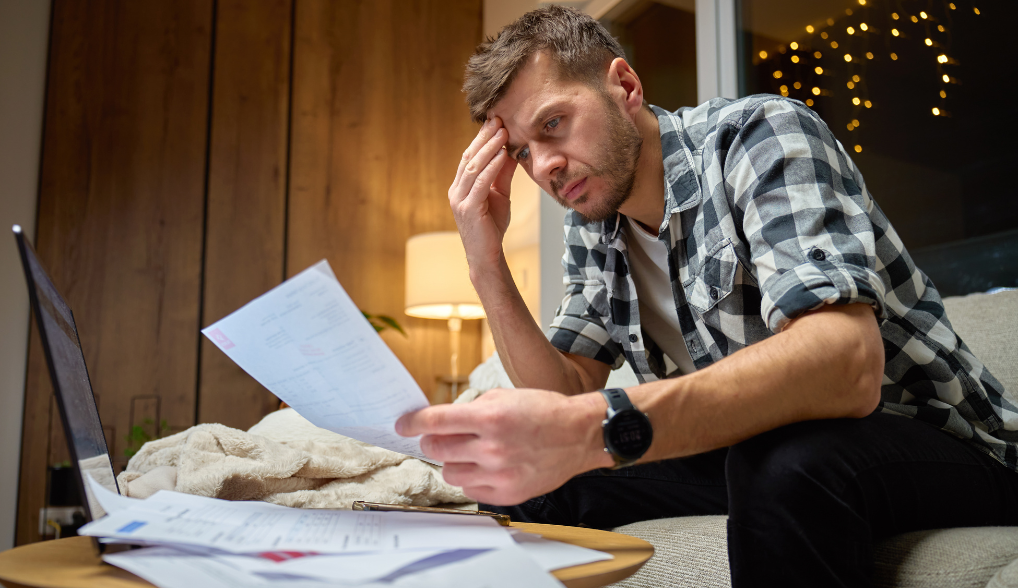

Money stress has a way of following you everywhere: it can affect your sleep, your relationships, and your ability to concentrate at work. You're not imagining it, and many Canadians are facing the same challenges.

42% of Canadians say money is their top source of stress, more than health (21%), relationships (17%), and work (17%). The rising cost of living in Canada, housing pressures, growing debt loads, and wages that can't seem to keep pace have pushed many people to a breaking point. If you've been lying awake running numbers in your head, that's a sign that financial stress is taking a real toll on your well-being.

While financial stress can feel overwhelming, it can be manageable. It takes both practical steps and a bit of self-compassion to work through it. Here's what you need to know.

Financial stress is emotional and physical tension triggered by money worries. It shows up as a sense of dread when you think about how to cover your bills, a tight chest when you open your bank app, or a general feeling of being stuck with no clear way forward. Financial stress can also lead to avoidance of checking your bank account or opening bills until it’s absolutely necessary.

It isn’t just for those having trouble making ends meet, either. Financial stress can show up even if you’re meeting your financial obligations due to uncertainty, a lack of savings, or fear of future financial challenges.

And for many Canadians right now, that feeling is hard to shake. Grocery prices are the top external stressor for 64% of Canadians, with inflation affecting 54% and housing costs weighing on many others. When there's no financial cushion to fall back on, any unexpected expense can tip the balance.

Financial Stress vs. Financial Anxiety

Financial stress and financial anxiety are related but different. Financial stress is usually a reaction to something specific: an unexpected car repair, a missed payment, a job loss. It tends to ease once the immediate situation is resolved or a plan is in place.

Financial anxiety is more persistent. It's the worry that something will go wrong even when your balance looks okay; a sense that financial disaster is always around the corner. This can sometimes develop into what's called money dysmorphia: a distorted view of your financial situation in which you feel "broke" even when you're not, often fueled by comparing your life to what you see online.

Both are real, both are worth taking seriously, and both respond well to the strategies below.

Common Causes of Financial Stress in Canada

The most common drivers of financial stress include:

The rising cost of living.

High housing and rent costs.

Accumulated debt (particularly credit card debt).

Unexpected expenses with no emergency savings to cover them.

Wages that haven't kept pace with inflation.

Irregular income, such as from self-employment or gig work.

Employment instability, such as contract workers.

How Does Financial Stress Affect Your Health?

Financial stress isn't just a mental burden; it has real physical effects. Those experiencing high financial strain are twice as likely to report poor overall health.

When you're under money stress, your body responds the same way it does to any perceived threat: it releases cortisol and adrenaline, which can raise your heart rate and blood pressure. Over time, that chronic activation wears the body down.

People facing high debt pressure are four times as likely to suffer from sleep problems, headaches, and other illnesses. Sleep disruption is one of the most common effects, with nearly 35%of Canadians reporting difficulty sleeping over money worries.

Chronic financial stress can also affect financial decision making, leading to avoidance behaviour or impulsive financial decisions that worsen the situation.

The connection between mental health and finances is well-established. Financial stress is a leading driver of anxiety, depression, and burnout. It can also spill into your relationships: anRBC 2024 Relationships and Money Poll found that money is a source of stress for more than three-quarters of Canadian couples, and the cause of arguments for three in five.

These are normal, understandable reactions to an overwhelming situation. They're also a signal that it's time to take action.

Tips for Dealing With Financial Stress

Managing financial stress requires two things to work together: addressing how you feel and taking concrete steps to improve the situation. Here's where to start.

Acknowledge It and Get a Clear Picture of Your Finances

The most common mistake people make when they're under financial stress is waiting too long to face the numbers. Avoidance feels protective in the moment, but it lets the problem grow.

The first step is simple: list your income, debts, and monthly expenses without self-judgment. You don't need a perfect system, just a clear picture of where things stand.

Create a Sustainable Spending Plan

Once you know where your money is going, the next step is building a plan that actually sticks. We encourage an approach called Sustainable Spending—a budgeting strategy designed for long-term financial health, not just short-term fixes.

It works through three simple steps, called the ABC method:

Analyze: Look at what's coming in and what's going out. Are you spending more than you earn?

Brainstorm: Think about ways to improve your cash flow, whether that's trimming expenses, boosting income, or setting a clear priority like paying down debt.

Change: Commit to one meaningful adjustment. Small shifts, done consistently, add up over time.

If you want structured support putting the ABC method into practice,Credit Canada GOLD is our financial coaching program built around sustainable spending. It combines behavioural science with one-on-one coaching to help you get out of debt for good.

Unlike rigid percentage-based frameworks, sustainable spending meets you where you are. According toStatistics Canada's Survey of Household Spending, shelter, food, and transportation alone account for nearly 64% of average household spending, meaning many Canadians are already stretched before anything else is factored in. Sustainable spending works with that reality rather than against it.

If you're tracking your expenses and aren't sure what to do next, we break downhow to create a monthly budget step by step. You might be surprised by how small regular purchases add up.

Using a budget planner can also help you identify patterns in your spending and spot areas where small changes may free up additional cash flow.

Build an Emergency Fund

Having a financial cushion is one of the most effective ways to reduce ongoing money stress. Aim for three to six months' worth of essential expenses, but even setting aside $1,000 can stop a single bad month from turning into a credit card spiral.

Start small. Automate a modest transfer right after each payday, even $25 or $50, so the savings happen before you have a chance to spend it.

Pay Down Your Debt

High-interest debt, especially credit card debt, can be a significant driver of financial stress for many Canadians. Fortunately, there are two methods that can help you pay off debt faster.

Focusing on your highest-rate balances first (the "avalanche" method) reduces the total interest you pay over time and can accelerate your progress. Alternatively, the “snowball” method focuses on paying off your smallest balances first, which can help build momentum and motivation as you work through your debt. While the avalanche method saves more interest mathematically, both are valid strategies. The best one for you will be the one you can follow consistently.

If the debt feels too large to manage on your own, speaking with a certified Credit Counsellor can help. They’ll review your financial situation and give you personalized, non-judgemental advice on the best way to move forward. This might include a Debt Consolidation Program (DCP), also called a Debt Management Program (DMP), or, in some cases, bankruptcy.

Ready to look at your options? Speak with one of our certified Credit Counsellors to explore what's available to you.

Find Ways to Increase Your Income

Sometimes financial stress persists because expenses have simply outpaced what's coming in. That's where the Brainstorm step of the ABC method comes in, to explore whether there's room to grow your income: a side project, extra hours, or renting out a room can all shift your cash flow in the right direction.

The same step applies to the expense side. Subscriptions and automatic payments have a way of quietly accumulating, and revisiting them is often easier than people expect. It's also worth shopping around on recurring bills like insurance, cell, and internet plans. Providers regularly offer better rates to new customers, and a quick comparison can free up meaningful room in your budget.

Talk to Someone

Isolation makes managing financial stress worse. Talking openly about what you're going through, whether with a trusted friend, a family member, or a professional, can break the cycle of shame and give you a clearer perspective.

It also helps in practical terms: your creditors may have hardship programs or payment deferral options you don't know about. You won't find out unless you ask.

Mike Bergeron, Counselling & Client Services Manager at Credit Canada, puts it this way: "Reaching out for support when you feel stuck isn't a sign of failure; it's an empowering step toward moving past what's holding you back. I don't know a single financial professional who wouldn't want to help someone if they had the opportunity. Allowing yourself to be vulnerable and starting a conversation with your bank, financial advisor, or a Credit Counsellor can make a meaningful difference."

Take Care of Your Mental and Physical Well-Being

Financial stress takes a toll on your body, and managing that toll matters. While taking care of your physical and mental health doesn’t directly solve your financial problems, it can improve your clarity and give you the energy you need to address them.

Regular exercise, even a short daily walk, helps regulate the stress response. Mindfulness and deep breathing can interrupt the anxiety spiral before it takes hold. Prioritize sleep and limit how much financial news you consume if it's making things worse.

Social connection matters too. Spending time with people who support you doesn't cost money and can help reduce feelings of stress, isolation, and overwhelm.

Seek Professional Help

There's a point where self-managed tips aren't enough, and recognizing that point is a sign of self-awareness, not weakness.

According to Bergeron, "When financial stress starts to feel overwhelming or debilitating, that's a strong signal to reach out and begin a conversation with a credit counsellor. Everyone experiences and manages stress differently, and there is no judgment, only support. Recognizing when things are heading in the wrong direction and seeking help before they worsen is a sign of strength, not weakness."

If any of the following apply to you, it's worth talking to someone:

You're losing sleep regularly because of money worries

You're using credit cards to cover rent, groceries, or utilities

You're only making minimum payments, and the balances aren't shrinking

Money stress is causing serious strain in your relationships

Self-managed tips

Credit counselling

Best for

Manageable debt, early stress, building habits

High debt load, persistent stress, no clear path forward

What it involves

Budgeting, saving, and debt repayment strategies

Certified Credit Counsellor reviews your full financial picture and options

Outcome

More control and better habits over time

Structured plan, potentially reduced interest, professional support

Credit Canada offers free, confidential support to Canadians regardless of income. Get expert advice, a clear path forward, and judgment-free support whenever you're ready.

Contact us or call 1 (800) 267-2272 to speak with a certified Credit Counsellor for personalized guidance.

Or, if you'd rather start on your own time, chat withMariposa, our AI-powered debt management agent, to explore your options.

Frequently Asked Questions

Have questions? We are here to help.

How does financial stress affect mental health?

Financial stress is a leading driver of anxiety, depression, and burnout. It can also cause cognitive fatigue, making it harder to focus, sleep, and make clear-headed financial decisions, which can deepen the cycle of stress if left unaddressed.

What are the most common causes of financial stress in Canada?

The biggest drivers right now are the rising cost of groceries and housing, accumulated debt (especially credit card balances), stagnant wages, and a lack of emergency savings. According to the FP Canada 2025 Financial Stress Index, 42% of Canadians say money is their top source of stress, ahead of health, relationships, and work.

What is the difference between financial stress and financial anxiety?

Financial stress is a direct reaction to a specific problem: a bill you can't cover, a job loss, an unexpected expense. Financial anxiety is more persistent, a chronic worry about money that lingers even when your current situation is stable, often focused on what might go wrong in the future.

How can I reduce financial stress quickly?

The fastest way to regain a sense of control is to get a clear picture of your finances: write down your income, debts, and monthly expenses without judgment. From there, even small steps like automating a modest savings transfer or calling a creditor about a hardship option can shift the feeling of being stuck.

When should I seek professional help for financial stress?

If you're regularly losing sleep, using credit to cover basic necessities, making only minimum payments with no progress, or feeling like there's no clear path forward, it's time to talk to someone. Credit Canada offers free, confidential credit counselling to all Canadians. Speak with a certified Credit Counsellor whenever you're ready.

Doris Asiedu • Author

Doris is an experienced Credit Counsellor, who specializes in Debt Consolidation, and budgeting help. She has been working on her personal mission of helping people in managing their money since 2006.

Reviewed by

Alexandra Rodriguez Bernal

• Credit Counsellor and Education Lead

X

Related Articles

I Made a Bad Financial Decision: What Now?

Have you ever kicked yourself after a bad financial move? We’ve all been there. Whether it’s an extravagant purchase on your credit card that you regretted later or a poor stock ...

The Surprising Link Between Finances and Mental Health

You’ve heard the phrase “money can’t buy happiness.” The phrase is nuanced by related results of money, like better access to personal care, shelter, entertainment, food, and ...

Financial Anxiety: How to Stop Worrying about Money

Financial problems can affect almost anyone—even people who make a lot of money and have a stable career may experience the occasional bit of anxiety about their finances. While ...