Frequently Asked Questions

Have questions? We are here to help.

Your credit report provides a comprehensive view of your financial history. You might see regular mortgage payments, car loan payments, and even a record of your first credit card. But what do those accounts, inquiries, and public records mean? How does all this affect your credit score?

Around half of Canadians are unsure of how their credit score is calculated. Millions of people are making financial decisions, like applying for mortgages or credit cards, without knowing what lenders actually see during an application review.

Understanding the facts about your credit report is more than just knowing a number. It's a detailed record of your financial history that gives you the power to spot errors, catch fraud early, and even improve your current financial standing by making informed changes in how you use credit.

*Note: Some of the images used below were taken from an Equifax credit report and are only meant to be used as helpful examples. Yours might look slightly different if you obtain your report from TransUnion.

A credit report is a statement about your loan history, credit activity, and credit account status. It acts as your financial report card for creditworthiness and debt management only, as credit reports don't include details on personal investments, savings, income, net worth, etc.

Lenders can access your credit report to help them decide whether you’re reliable enough to lend to. Potential employers and landlords may also access your credit report if given permission.

Your credit report contains the following insights into your historical and current credit scenario.

|

Report Section |

What It Contains |

Why It Matters |

|

Personal Information |

Name, address history, date of birth, and employment. |

Confirms your identity. |

|

Credit Accounts |

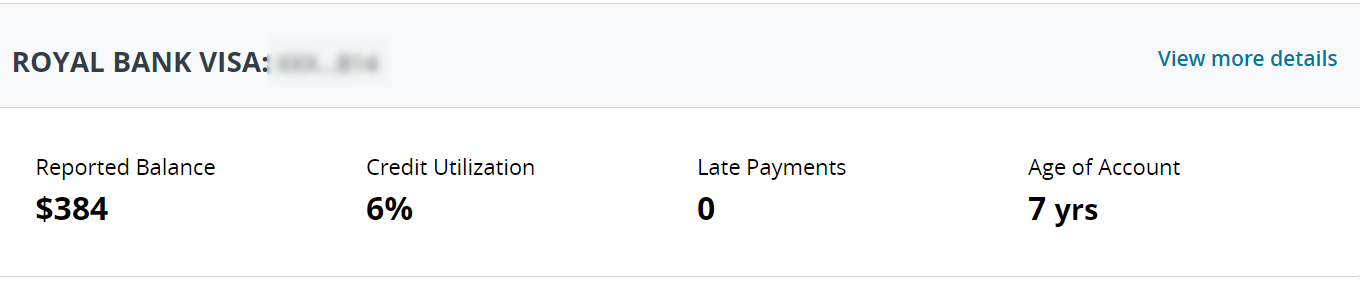

Revolving accounts, including credit cards and lines of credit. As well as installment-type accounts, which includes car loans, personal loans, and mortgages. |

Shows how you manage different types of credit. |

|

Payment History |

Record of on-time, late, or missed payments for each account. |

One of the most important factors in your credit score; demonstrates reliability. |

|

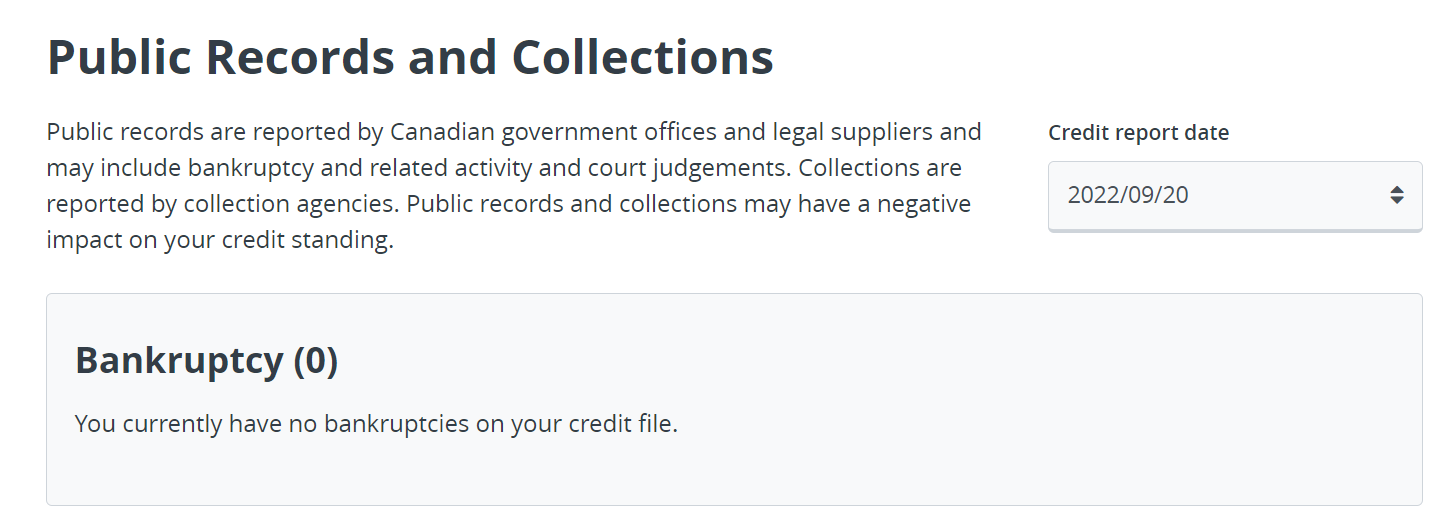

Public Records |

Bankruptcies, consumer proposals, court judgments, liens. |

Indicates serious financial difficulties that significantly impact your score. |

|

Inquiries |

Record of who has accessed your credit report and when. |

Too many hard inquiries can lower your score temporarily, as it may raise concerns for lenders, suggesting you are overly eager for credit by applying for multiple accounts. |

|

Collections |

Unpaid debts sent to collection agencies. |

A major red flag that stays on your report for six to seven years. |

Credit bureaus have personal details such as your phone number, email addresses, reported addresses, birthdate, and full name. All this shows up on your credit report.

Accounts include personal loans, lines of credit, mortgage loans, credit cards, and other credit accounts that require a credit check.

Most payday lenders and Buy Now, Pay Later (BNPL) providers do not report regular payment activity to the credit bureaus. As a result, these accounts typically don’t appear on your credit report or help build credit — unless the debt is sent to a collection agency, in which case it can be reported and negatively affect your credit.

You’ll probably see the most accounts under the “Revolving Credit” section. These accounts have a limit and a minimum payment. If you’re late on your credit card payment, you’ll see it here.

Public records are credit-related legal matters viewable by the public. We’re talking:

Most of these items will stay on your credit report for a minimum of six years. Fortunately, collections entries are automatically removed from your credit report once they expire after six years.

A pre-approval or personal inquiry won’t affect your credit score. These are called soft inquiries.

What about a lender assessing your creditworthiness for a mortgage or car loan? That’s a hard inquiry, and it would slightly affect your credit. Too many hard inquiries can lower your score.

If you’re wondering what will impact your credit score, Equifax makes it simple by including a “May Affect Scores” column that indicates whether each inquiry affects your score.

Reading a credit report becomes easier once you understand how it’s written. Let's break down what you're actually looking at.

Each credit account on your report has a code that tells lenders how you've managed it. The most common system uses a letter-number combination:

Letter Codes:

Number Codes (0-9):

The most common mistake Canadians make when reading their credit report is avoiding looking at negative information, but this isn’t the solution for fixing credit issues. Taking proactive steps, like working with a certified Credit Counsellor or arranging a payment plan with your lender, can gradually repair your credit.

Mistakes happen more often than you'd think. Common errors to watch for include:

Canada’s two credit bureaus are Equifax and TransUnion, and your reports for each may differ slightly. Not all creditors report to both bureaus, and each formats information differently.

That's why we recommend checking both reports annually to catch errors that might appear in only one of them. Your rights allow you to request one free credit report per year from both bureaus.

Here’s the thing: credit bureaus don’t offer a public formula about how they calculate your credit. However, lenders typically assess the following:

Finding and fixing errors on your credit report can be frustrating, but you have the right to dispute them. Follow these steps to correct your credit report:

Collect documentation that proves the error, including bank statements, receipts, and correspondence with creditors. The more evidence you have, the stronger your case.

File a dispute directly with the bureau whose report contains the error. You can typically do this online, by phone, or by mail. Be specific and include copies of your supporting documents.

Both bureaus must investigate your dispute within 30 days. If they determine the information is incorrect, they'll update your report.

While the credit bureau investigates, contact the creditor who reported the incorrect information. Explain the error and provide your evidence. They may be able to resolve it more quickly.

If the investigation doesn't resolve the error, you can escalate your complaint to the Financial Consumer Agency of Canada (FCAC) or your provincial consumer protection office.

Be cautious of companies that promise to "fix" your credit for a fee or claim they can remove accurate negative information.

Understanding your credit report is important, and there’s help available if you have questions. The more informed you are about your personal credit score, the fewer challenges you might face when you seek credit.

Consider seeking professional help if you’re overwhelmed and want your credit report explained, planning a major purchase, or feeling the weight of financial stress.

Credit Canada’s certified Credit Counsellors offer free, confidential support to help you understand your credit report and develop an action plan to regain your financial control with confidence. Contact us online or call 1 (800) 267-2272 to get started.